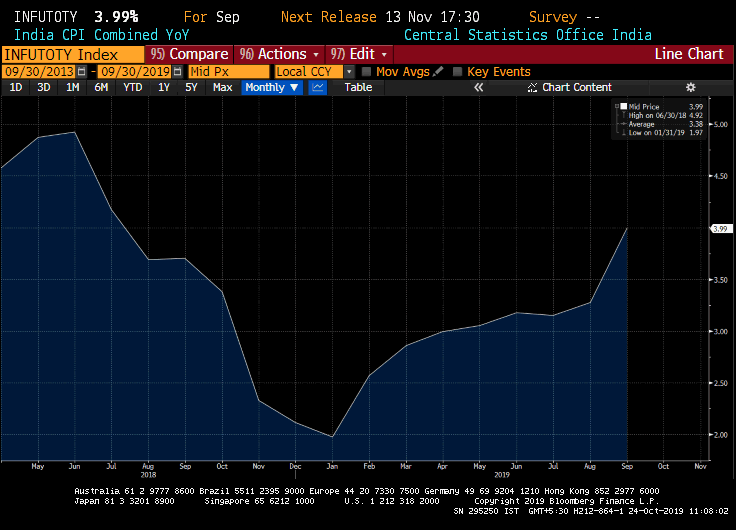

The rupee is trading in a narrow range amid the absence of fresh trigger in the market. India’s

macroeconomic data have turned favourable. The CPI has increased to 3.99% in September,

from 3.21% in the previous month. However, it still remains within the comfort zone of the

RBI. A favourable monsoon and decline in crude oil prices may keep inflation under control of

the RBI. After a sharp surge in September, crude oil prices have fallen sharply after Saudi

Arabia’s crude oil production restored to normal. The trade deficit has narrowed to $10.86 billion

in September, from $13.45 billion in the previous month. Current account deficit has also

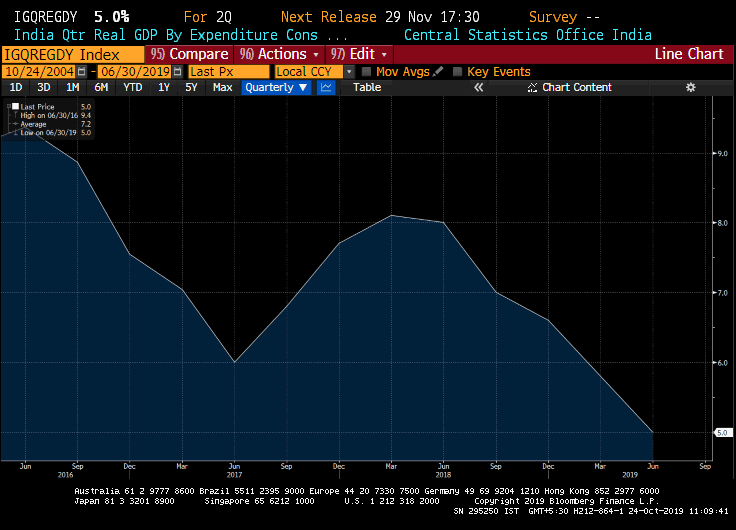

narrowed sharply. But GDP and industrial production have declined sharply. Hence the RBI is

cutting interest rates sharply and is expected to cut further to revive GDP growth.

INDIA’s CPI

Source: Bloomberg

Source: Bloomberg

The performance of key US economic data is falling. The trade conflict between the US and

China has slowed global and US economic growth. Manufacturing PMI across the world is faltering due to the ongoing trade war and dull demand. Companies are blaming the slowdown on Trump’s tariffs on Chinese goods. This seems to have escalated into a full-blown trade war with China, which has responded with its own tariffs. As the US presidential election of 2020 is approaching, Trump is increasing his pressure on China to correct trade practices. The trade conflict is leading to technological conflicts as well. Hence the real deal between the US and China is unlikely. The IMF has cut the global growth forecast for 2019 and 2020.

INDIA’s GDP GROWTH

Source: Bloomberg

Source: Bloomberg

As a result, the Federal Reserve has cut interest rates twice this year. With the second cut, it

seems that the economy is slowing down more than the Fed’s anticipated. The pressure on the

Fed is growing as the ECB has cut interest rates and announced a QE, and that has weakened

the euro. Hence, Trump is piling on the pressure on the Fed to cut interest rates further, faster

and deeper. The overnight borrowing cost in the money market that banks and corporations

depend upon for their daily cash needs surged sharply to 10%. To calm markets, the Federal

Reserve Bank of New York stepped in, injecting billions of dollars. It was the first time such an

action has been taken since the 2008 financial crisis.

Hence, some investors view this as the Fed introduces another round of quantitative easing. The US House of Representatives has initiated a preliminary inquiry into whether to proceed with a formal impeachment investigation of US President Donald Trump, a move that could negatively impact risky assets. There is a fear of recession in the US due to yield curve inversion. The Brexit drama continues to unnerve investors. With the setback in the UK parliament, the UK Prime Minister Boris Johnson might announce snap election and ask the EU for another extension to secure a better deal.

The Chinese economy is slowing down sharply due to the trade war. Though the Chinese yuan has stabilized, there is still fear of sudden yuan depreciation. The possibility of China devaluing its currency (similar to August 2015) cannot be ruled out as the currency war is brewing in the other major economies. Hence the domestic and global factors will give further direction to the rupee. Overall, the near term outlook of the rupee is mixed.

TECHNICALS

On the weekly chart, USDINR currency pair is trading above the 50-SMA and above 14-EMA

also. USDINR price has made multiple attempts to break below a very strong support level at

70.50 but bounced back sharply from lower levels around 70.55 to 70.60 which indicate buying

at lower levels. However, on a daily chart, price is trading below 50-SMA and 14-EMA and MACD

indicator is also showing negative crossover which adds weakness in prices. Very strong

support is placed at 70.50 and resistance will be coming at 71.40 which show USDINR may

remain within the range of these levels. A break below 70.50 will open up further downside

and if this support level remains intact then upside bounce expected till 71.30 in the near term.

Author: Rushab Maru – Research Analyst – Currency & Commodity, 2nd November 2019