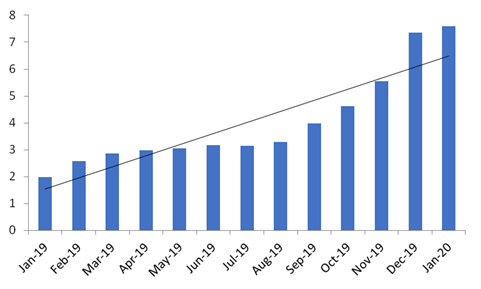

India’s macroeconomic conditions continued to worsen. According to the latest data, the CPI has increased to 7.59% in January, from 7.35% in the previous month. The inflation has increased on account of higher food prices due to unseasonal weather pattern in the country. Industrial production has once again contracted in December and fell by 0.3% in December, from the growth of 1.8% in the previous month. The government has revised up its fiscal deficit forecast for the current financial year due to shortfall in the revenue collection.

India’s CPI inflation

Source: Bloomberg

The government has projected a fiscal deficit at 3.8% of GDP in FY20 against the previous projection of 3.3%. The government has projected a fiscal deficit at 3.5% of GDP for FY21. India’s fiscal deficit has already hit 132% in April to December period. This is a matter of concern for the market. External environment remains quite uncertain; this may have ramifications on the export performance. The GDP growth has been subdued. Hence with the high inflation and slowdown in the GDP growth, the RBI’s job has become difficult. Earlier this month, the RBI kept the repo rate unchanged at 5.15% in the monetary policy meeting and it may continue to maintain status quo for few more months.

On the other hand, the spread of coronavirus has sent shockwaves across the global financial markets. The Chinese stock market has plunged sharply on fear the virus may further slow down economic growth in China. This has rattled financial markets across the globe. According to the latest updates, the coronavirus has spread to South Korea, Iran, Italy, Japan, Singapore and many other countries. This may have serious repercussion on the global supply chain. Hence this pandemic has sent the dollar index sharply higher. This may have huge ramification on the emerging market currencies including the rupee.

The trade deal between the US and China is also in jeopardy. The rapid spread of coronavirus in China could sharply curtail its ability to meet the purchasing target of the trade deal struck with the US. Hence the trade tension may once again surface. As a result, the yuan may come under pressure in coming sessions. The Fed has kept interest rate unchanged in the recent monetary policy meeting. But a sharp drop in the US Treasury bond yields in recent sessions suggest that the Fed may need to cut interest rates. Hence, there are domestic as well global challenges lie ahead for the rupee. Overall, the outlook of the rupee is bearish for the medium term.

Author: Mr. Rushabh Maru, Research Analyst – Currency & Commodity (Investment Services), 28th February 2020